Panupong Piewkleng

[Limbach Holdings] does not need to strike successive crowning achievement to reach a $30 share rate; 12% profits development in the ODR section, decreasing GCR profits, no margin growth, and modest multiples suffice to make the business a multibagger over the next 5 years” – Me, in my last Limbach post

Limbach Holdings ( NASDAQ: LMB) stays a multibagger in the making. The business’s stock rate is up 130% because my last post was released and I believe it is most likely to double once again in the next 3-5 years. LMB is growing its owner-direct relationships (ODR) at a sped up rate, enhancing its general-contractor (GCR) margins, and supporting its balance sheet for future acquisitions. In this post I will upgrade my LMB financial investment thesis and emphasize why I believe the business will flourish in the years ahead, even in a recessionary environment.

Business Updates

I am going to presume that readers are currently acquainted with LMB and the financial investment thesis I set out in my previous posts. With that in mind, there are a set of essential updates to highlight. Initially, LMB has a brand-new CEO. Long Time CEO Charlie Bacon has actually stepped down from the function and passed it on to Michael McCann, the business’s Chief Operating Officer. McCann has actually worked carefully with Bacon to focus the business on growing ODR profits, and I anticipate the long-lasting prepare for LMB to stay the exact same after the shift.

2nd, LMB changed their 2023 (and beyond) forecasts on the last business teleconference. Earnings expectations were increased to in between $490mm and $520mm, with profits equally divided in between the ODR and GCR sections. This boost indicates 16% development in ODR profits. I was likewise pleased to see that management was comfy raising GCR section margin expectations to a series of 12% -15% (up from 12% -13%). As assured, LMB is growing ODR profits, enhancing GCR margins, and producing favorable EBITDA and capital.

Development Towards the Financial Investment Thesis

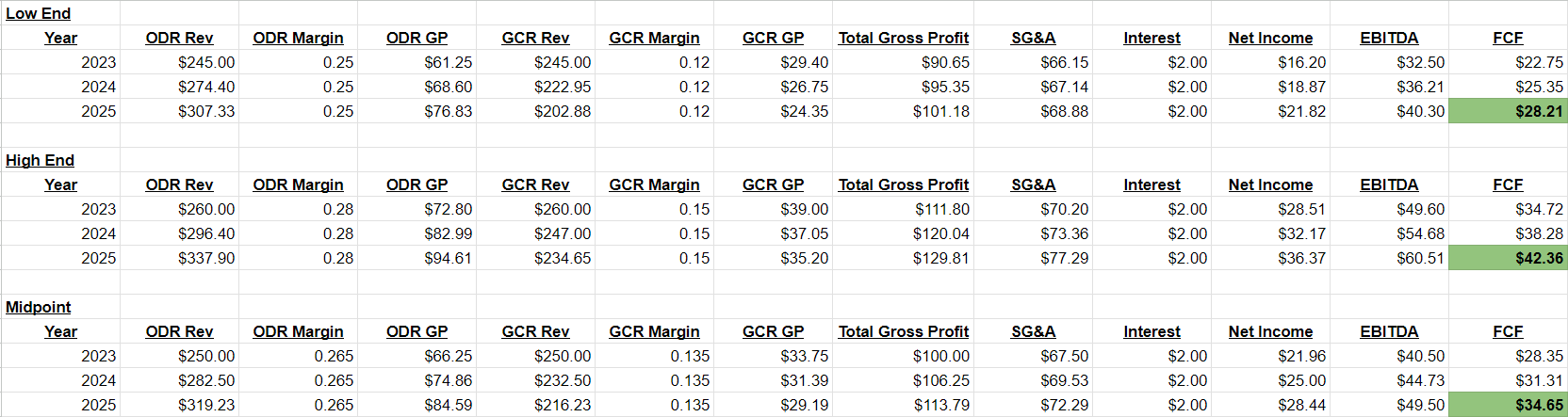

I have actually upgraded and broadened upon the design I provided in my previous post. I included management’s 2023 assistance ( source), included a totally free capital price quote, and detailed 3 various circumstances: the low-end of management’s price quotes, the high-end of their price quotes, and the midpoint of their price quote varieties. All dollar worths remain in millions.

Limbach 3-Year Financial Quotes (Author’s Spreadsheet)

If management can satisfy the midpoint of its assistance over the next 3 years, the business will be producing approximately $50mm in EBITDA and $35mm in constant totally free capital in 2025. LMB produced almost $35mm in FCF this previous year, however the worth was pumped up due to the timing of shifts in working capital. Using my normal standard target of a 10x FCF evaluation, this would provide LMB a forecasted market cap of $350mm, precisely double today’s present market cap of $175mm. This equates to a target share rate of $32.50.

Will LMB’s Development be Thwarted by an Economic downturn?

The marketplace is worried about an impending economic crisis, however I believe an economic downturn will assist LMB more than it will injure it. I believe this for 2 factors. Initially, LMB’s consumers depend on the business to support mission-critical systems. To price quote brand-new CEO Michael McCann from last quarter’s teleconference:

Limbach is likewise extremely concentrated on being disciplined in dealing with consumers where their systems are mission-critical and require no matter the macroeconomic environment. In these kinds of structures, the owners can postpone big capital investment, however they can’t prevent instant repair work.” ( source)

When you run an information center or a health center, you can’t pay for to have your cooling decrease for a prolonged time period, so upkeep and emergency situation repairs stay a concern even an economic downturn. Due to the fact that LMB has actually concentrated on growing direct relationships with structure owners, they will stay the very first call that the structure owners make when they require help. If business are required to postpone brand-new building and construction or significant upgrade work due to capital restrictions brought on by an economic downturn, it indicates they might require to all of a sudden invest more into repair and maintenance on their existing systems. This makes them prospective brand-new consumers for LMB’s services.

2nd, a hard macroeconomic environment might provide LMB with accreditive acquisition chances. The business had a net money position at the start of 2023 ($ 36mm in money versus $32mm in overall financial obligation) and is currently searching for takeover prospects. If other services in nearby markets (especially those concentrated on brand-new building and construction) start to have a hard time in a financial decline, they might be more open up to a buyout and have less utilize in working out a list price. LMB has actually currently shown its M&An abilities with its acquisition of Jake Marshall at the end of 2021. LMB paid $19mm web of money got for Jake Marshall, and in 2022 the department produced $63mm in profits, $9.7 mm in gross earnings, and $3.7 mm in earnings. I’m extremely delighted to get an organization with development potential customers at a cost that is just 5 times profits. If extra acquisition chances provide themselves in an economic downturn, LMB will have the monetary versatility and acumen to make the most of the circumstance.

Dangers

While an economic downturn would likely assist LMB grow its service and upkeep profits, it is likewise possible that it would minimize the variety of new-construction jobs they are granted. If LMB’s consumers put capital investment and growth intend on hold, that lost profits will just be partly balanced out by a boost in service profits. That being stated, I do not anticipate brand-new building and construction to entirely fall off a cliff. Federal and state federal government costs programs connected to 2021’s bipartisan facilities legislation are simply starting in earnest, and the passage of the CHIPs costs and Inflation Decrease Act will supply more assistance to a lot of LMB’s existing and prospective consumers.

I do not see there being liquidity threat for LMB in an economic downturn. The business has actually gotten to a net-cash position on their balance sheet and has more than $20mm in offered liquidity on their credit center. I do not anticipate this to be a concern anyhow, as the business has actually convincingly relocated to producing favorable totally free capital and should not require extra credit unless an acquisition happens.

Conclusion

If the United States economy handles to prevent falling under an economic downturn, then I anticipate LMB to continue its consistent and constant development. The business is on track to produce significant and constant capital, which I anticipate to equate into a share rate north of $30. If an economic downturn emerges, I anticipate LMB to be able to grow its consumer base even quicker and possibly have the ability to get a good deal on an acquisition. LMB is the 3rd biggest position in my portfolio and I am comfy keeping it an extremely weighted, even in the face of a prospective economic crisis.

Editor’s Note: This post was sent as part of Looking for Alpha’s Finest Financial investment Concept For A Prospective Economic downturn competitors, which goes through April 28. This competitors is open to all users and factors; click on this link to learn more and send your post today!