The real estate market was insane once again recently. Home loan rates fell as the banking crisis worsened and purchase application information grew for the 2nd week in a row, however the huge concern is: Did we struck the seasonal bottom in real estate stock?

Here’s a fast rundown of the recently:

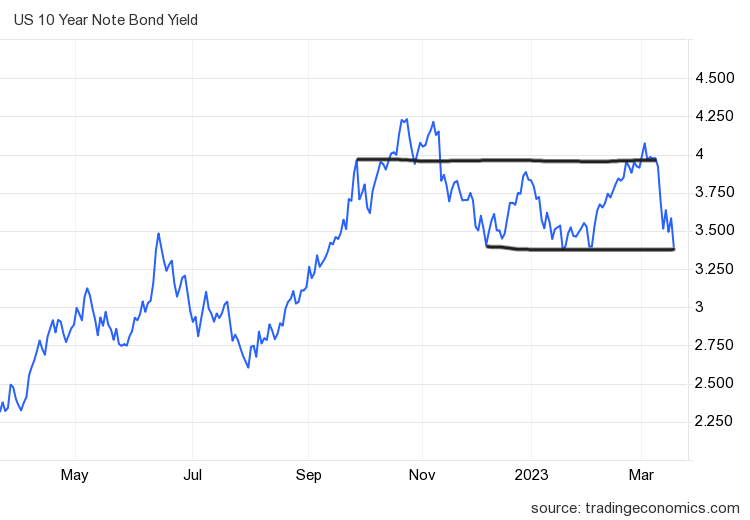

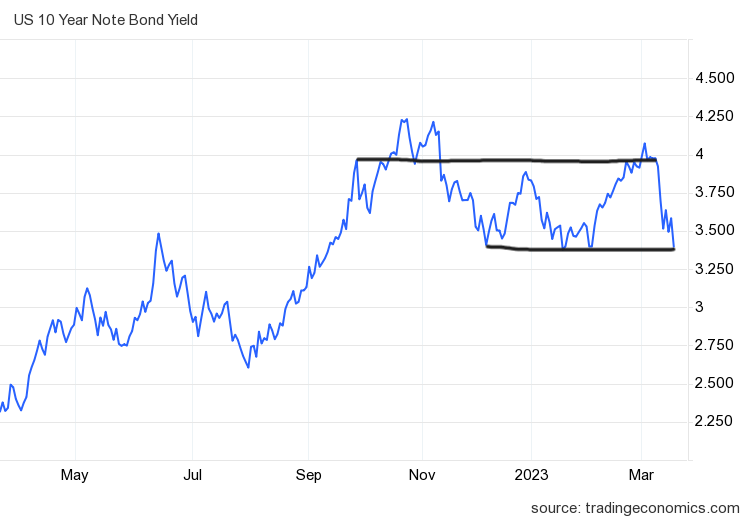

- The 10-year yield had a roller-coaster week, therefore did home loan rates, however the 10-year yield held its crucial line, and home loan rates ended at 6.55%.

- Weekly stock increased by 1,734. New noting information collapsed, however we are putting an asterisk on that information line for today.

- Purchase application information increased 7% weekly, still down 38% year over year.

10-year yield and home loan rates

A nationwide banking crisis while the Federal Reserve raises rates and decreases its balance sheet seems like a poor mixed drink for economics, however that is specifically what we are handling today. As I compose this post, I see news that even Warren Buffet has actually been asked to chime in on how to handle this crisis.

So, we can now include a brand-new variable into the formula for 2023: What does a banking crisis imply for home loan rates?

In my 2023 projection, I stated that if the economy remains company, the 10-year yield variety ought to be in between 3.21% and 4.25%, relating to home loan rates of 5.75% to 7.25% If the economy gets weaker and we see an increase in unemployed claims, the 10-year yield ought to go as low as 2.73%, equating to 5.25% home loan rates This presumes the spreads are broad as the mortgage-back securities market is still really stressed out.

The financial information was okay recently. If we didn’t have the banking crisis, we would most likely simply concentrate on how firm the financial information was recently. GDP development was approximated at 3.2%, unemployed claims fell recently, real estate starts beat quotes and purchase application information revealed some development. Retail sales were somewhat listed below quotes, however we had favorable modifications, and commercial production was the same.

Recently’s 10-year yield took us to the crucial line in the sand.

Recently the two-year yield collapsed from a 5% level to under 4%. This bond market is yelling at the Fed to cut rates. Nevertheless, lots of Wall Street companies were banking on greater rates and got burned by the banking crisis. So, the marketplace is wild and the Fed may not care what short-term rates are doing now.

Home loan rates fell and ended the week at 6.55%, nevertheless, we see a great deal of tension in the monetary markets. Many individuals questioned why home loan rates weren’t lower on Friday; the response is that the banking crisis has actually worried the mortgage-backed securities market more than when bond yields was up to these levels last time.

So this is going to be an impressive week since we have actually integrated a brand-new variable into 2023 that wasn’t in the formula at the start of the year and the Fed fulfills on Tuesday and Wednesday.

I wish to see how the 10-year yield acts today. Can we get follow-through bond purchasing, which would take a direct chance at the low-level series of 3.21%? That would be a huge offer to me since it’s occurring with the labor market still doing OK.

We do not understand what news can occur at any 2nd to alter the landscape of the financial conversation till the monetary markets relax.

With the capacity of news worsening in the short-term, we require to be conscious that we can see some insane market prices in home loan rates and relocations in the 10-year yield. So, every day counts now throughout a banking crisis, as the world markets are attempting to bring back some order.

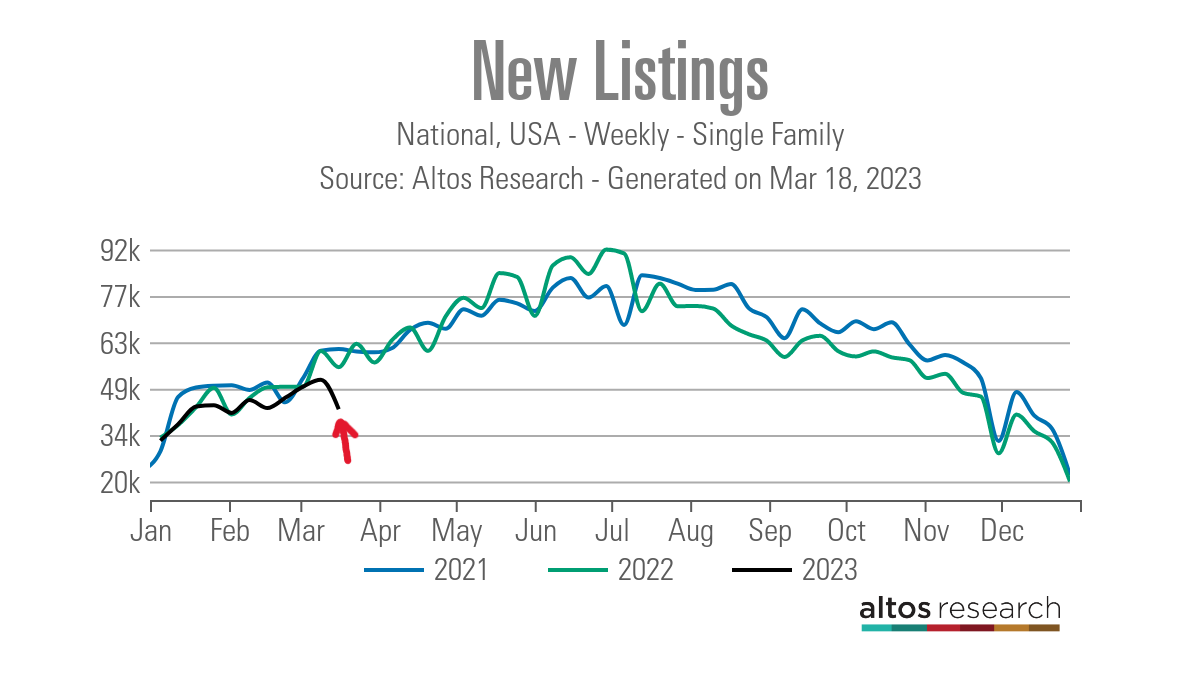

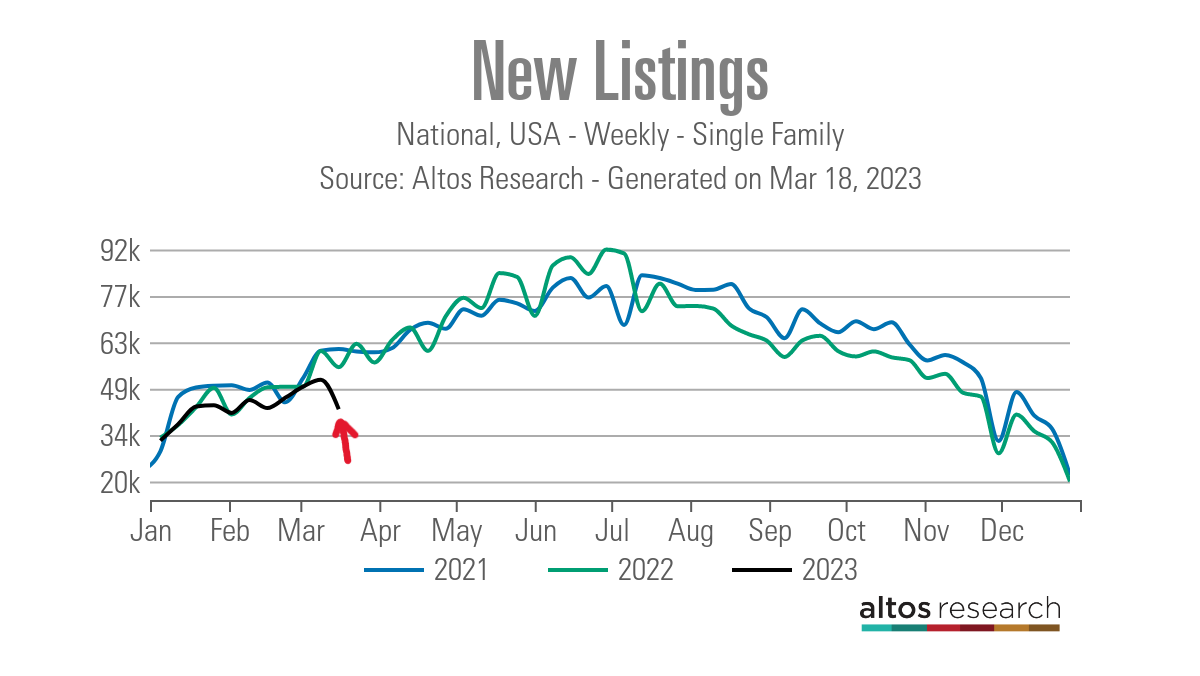

Weekly real estate stock

Taking A Look At the Altos Research Study information from recently, the huge concern is whether we are lastly beginning to see the seasonal boost in spring stock. On this front we have some great news and some problem.

Initially, we saw a somewhat increased variety of active listings, that made me rejoice! Last March is when we saw the seasonal bottom prior to stock removed, so I am hoping we get the exact same development in the information today, making it back-to-back years that we bottomed out in March. Although that’s not typical, it’s much better than what we saw in 2021 when we didn’t struck bottom till April.

- Weekly stock modification (March 10-March 17): Rose from 412,535 to 414,278

- Exact same week in 2015 (March 11-18th): Fell from 247,320 to 245,776

- The bottom for 2022 was 240,194

The seasonal boost in stock suggests more sellers can likewise be purchasers of houses and less bidding wars in specific parts of the nation.

Now the problem: brand-new listing information fell a lot today that I am putting an asterisk on today’s information till we see if this is a pattern or simply a one-off in the weekly information that can happen from time to time.

Likewise, we are developing a larger space in the year-over-year information. Previously in the year, we were on par and even somewhat greater some weeks than the previous 2 years. Now we are developing a larger space, as you can see listed below:

- 2021 60,904

- 2022 55,348

- 2023 42,407

For some historic referral, these were the weekly stock information in previous years:

- 2015 80,909

- 2016 84,647

- 2017 78,237

Now, this brand-new listing number can be one week of information that simply goes back to the pattern, which would be greater than this level. Or, like in 2015 at the end of June, when rates surged greater, we saw an obvious decrease in brand-new listings, because homes didn’t wish to note their houses with rates increasing.

This is something that I have actually spoken about previously– some house owners simply do not wish to purchase houses with home loan rates of 7% plus and choose to call it to stops. This is an issue when home loan rates move greater too rapidly, and it gets more difficult to make that huge life-long choice when the expense of real estate matters.

Let’s wait 2 more weeks and see if this brand-new listing pattern continues or simply goes back greater. I am hoping it’s simply a one-week occasion.

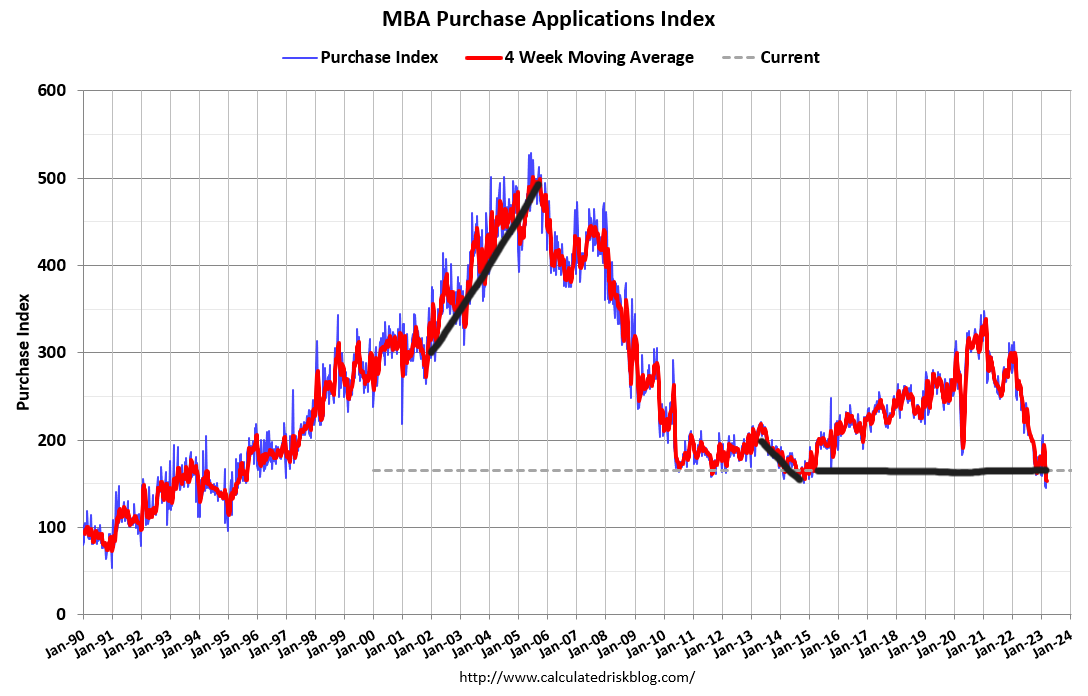

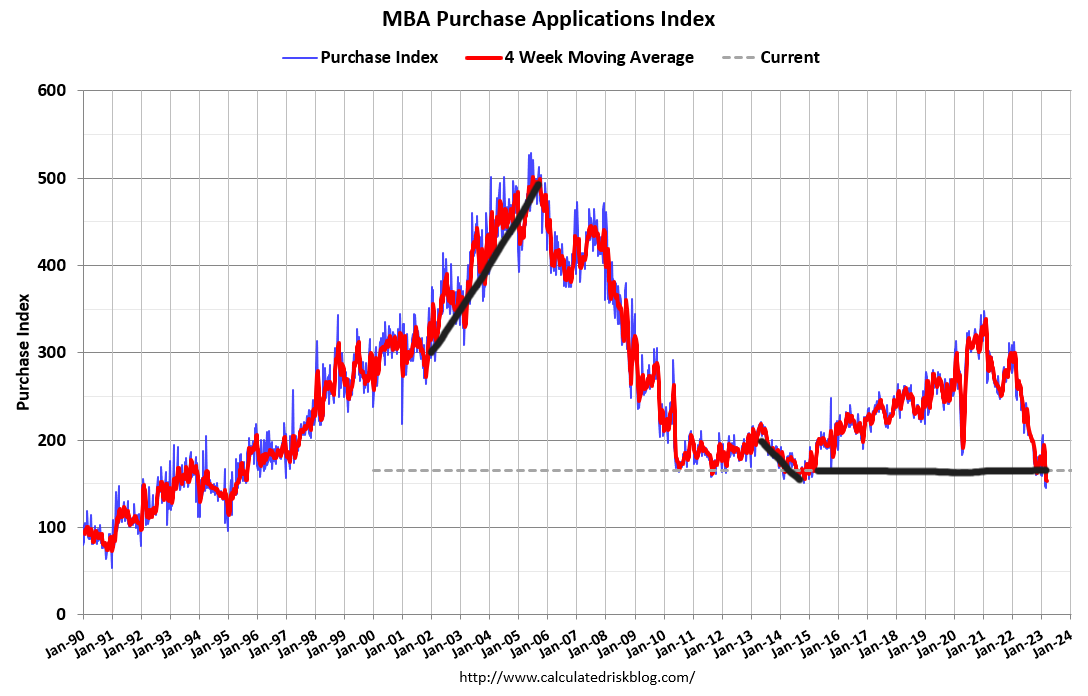

Purchase application information

Recently we improved news with another 7% week-to-week gain on purchase apps, and the year-over-year decrease likewise fell. Nevertheless, as I constantly tension, the bar is low here, so it does not take much to move the needle on application information when home loan rates move lower.

When rates surged from 5.99% to 7.10%, that offered us one month’s unfavorable information week to week, however the last 2 weeks have actually been favorable. We have actually had more favorable purchase application information than unfavorable because Nov. 9. Considering that this information keeps an eye out 30-90 days, today’s existing house sales report ought to see a bounce.

We require to be conscious of the information coming out later on in the year with the one-month decrease in this index. Nevertheless, you do not require to be a rocket researcher or have a Ph.D. in economics here to understand the real estate market is moving with where the 10-year yield is going, even with home loan spreads broad. So with all the drama we have today, let’s see if home loan rates fall even more today or whether the line in the sand holds.

The week ahead

Today we have existing house sales and brand-new house sales reports coming out, however to be dead truthful, financial information does not matter till we get control of this banking crisis scenario. While composing this post, news broke that UBS is purchasing Credit Suisse with federal government assistance and Flagstar will purchase Signature Bank possessions. In addition, the Fed revealed a

collaborated reserve bank action to boost the arrangement of U.S. dollar liquidity.

In times like this, market drama requires to relax initially prior to we can concentrate on the financial information. The Federal Reserve will satisfy today on Tuesday and Wednesday, and the Q&A part of this conference will be legendary.

Keep in mind that back in November Fed Chair Powell stated, “I do not have any sense we have actually overtightened or moved too quick.” Now, after all the emergency situation banking loaning programs and worldwide coordination to keep the banking system working, does he still think this declaration? I am hoping somebody asks him this direct concern.

Listening to what the Fed states today is crucial. We can focus straight on the real estate information, however the sound today will identify whether the marketplace thinks this banking crisis is under control or it’s stressing out of control, requiring the Fed and the federal government here and worldwide to do more to soothe the marketplaces down.