TennesseePhotographer/iStock through Getty Images

CBL & & Associates Residence ( NYSE: CBL) owns average shopping malls, still has the very same average management, and has excessive financial obligation relative to the quality of their properties. They left Ch.11 insolvency in November 2021 under an unreasonable reorganization strategy. Considering that I question the long-lasting practicality of CBL I would not be a purchaser of this REIT.

2020 Ch.11 Personal Bankruptcy

When taking a look at CBL & & Associates Residence you require to begin by taking a look at their 2020-21 Ch.11 insolvency case. I composed a variety of posts on CBL throughout their insolvency procedure, and I believed I would wait a couple of years before I composed another post to provide time to “get their act together” before composing a follow-up post.

Their insolvency reorganization strategy was unreasonable and ought to not have actually been validated by the court, in my viewpoint. While they did minimize their financial obligation, they left insolvency with excessive financial obligation. Financial institutions ought to not have actually gotten $455 million 10% protected notes as part of their healing. CBL did not raise $455 million in brand-new money from these notes – the notes were simply offered to the lenders as part of their healing for their claims. The truth is that the notes were provided so that the numerous claim classes would vote to accept the strategy that “talented” brand-new equity to both favored investors and typical equity holders. Financial institutions ought to have gotten 100% of the brand-new equity rather of 89% and they ought to have not been provided any notes, in my viewpoint. [Note: the remaining 10% secured notes were redeemed in May 2022 with funds from a new non-recourse secured loan that is half fixed rate (6.95%) and half variable rate (9.43% 3Q’23)]

The worth of the overall brand-new equity would increase, in theory, by $455 million without the issuance of $455 million financial obligation without getting money for that financial obligation. (Really, it is not a specific 1 to 1 worth since it would be changed based upon the capital structure optimization aspect, however that is beyond the scope of this post.) For that reason, by providing lenders brand-new financial obligation for their claims the outcome was simply increased debt/leverage for the brand-new CBL and not actually a boost in the worth of their healing bundle.

This strategy frustrated numerous unsecured noteholders who got less than complete healing while at the very same time, lower concern classes got a healing. Some favored investors, who got 0.043912176 of a share of brand-new CBL per favored share, were upset since typical equity investors got a healing of 0.005457723 of a brand-new share of CBL stock per old CBL in spite of the reality the favored investors did not get a complete healing for their claims. (I covered this concern in information in previous posts.)

One piece of proof that supports my assertion that they left insolvency with excessive financial obligation is a declaration consisted of in their 10-K that was submitted on March 31, 2022, just a couple of months after they left insolvency: “We presently do not have enough liquidity to satisfy these commitments as they end up being due, which raises considerable doubt about our capability to continue as a going issue.” What? They simply left insolvency a couple of months before the 10-K filing and they currently consisted of a “going issue” caution. The specified solution was “management means to re-finance and/or extend the maturity dates for such home loan notes payable.”

This “going issue” declaration was likewise unpleasant since in order for an insolvency strategy to be validated by the court under

area 1129( a)( 11 ) the “verification of the strategy is not most likely to be followed by the liquidation, or the requirement for more monetary reorganization, of the debtor or any follower to the debtor under the strategy …” These maturity concerns ought to have been resolved throughout the Ch.11 procedure even if the home mortgages were not straight part of the insolvency. While they were ultimately able to handle this “going issue” concern, this is simply another example of bad CBL management who did not “clean-up” all these concerns prior to leaving insolvency. Generally, the very same management, the Lebovitz household, that drove CBL into insolvency still runs this REIT.

Retail Renters

Among the very first products numerous shopping center REIT financiers take a look at is the list of their significant retail occupants to assist figure out the quality of the shopping center and the prospective lease rejections/defaults by having a hard time merchants who may declare Ch.11 insolvency in the future. CBL has primarily the common middle-market shopping center merchants – absolutely nothing upscale like Gucci or Prada.

Leading 25 Renters 2022 Based Upon Income

2022 10-K ( sec.gov)

It is fascinating to keep in mind that 2 significant anchor occupants did not make the leading 25 occupant list based upon profits. There are 17 JC Penney shop leases (CBL-owned shops) with 1,828,329 sq. ft. and 8 Macy’s ( M) shop rents with 905,442 sq. ft. I am unsure if the 7 Bed Bath & & Beyond closed shops (189,770 sq. ft.) have brand-new occupants yet. (I am presuming that a few of the $3.147 million uncollectable profits at the end of 3Q was connected to BBBY.)

There are a couple of merchants on their leading 25 list, such as Express ( EXPR) (30 stores/246,437 sq. ft.), and I have major issues that they will remain in insolvency within the next year or 2. If the economy deteriorates over the next couple of quarters, I likewise fret about JC Penney. (Note: for those thinking about following the liquidation procedure of retailers you ought to follow Copper Home CTL Go Through Trust (CPPTL), which is the trust that is liquidating numerous previous JC Penney shops.)

B and C Shopping Malls

I have actually remained in much of CBL’s shopping malls, and it appears in order to preserve capital they have actually been managing expenses by managing the quantity of upkeep labor expenditure. In B and C shopping malls I think customers endure these small upkeep issues, however the shopping malls are not inviting and frequently do not use a satisfying experience. To take on e-commerce, shopping malls require to be actually a satisfying experience – they are not.

There are regular assertions that these shopping malls and their associated parking lots/parcels may be able to be offered or partly cost brand-new advancements as the shopping center’s effectiveness ends. That is frequently simpler specified than achieved. Sometimes, any required zoning modifications or exemptions are simply rubber-stamped by city governments, however frequently there is regional opposition that postpones or perhaps eliminates these propositions. For instance, Pennsylvania Property Financial Investment Trust ( OTC: PRET), which is presently trading at $0.015 after changing for a reverse stock split, had a variety of propositions that fulfilled significant regional opposition that considerably affected this shopping center REIT. In one case they wished to develop an apartment on their residential or commercial property however there was significant opposition based partly on the predicted boost in sewage usage would put pressure on their existing close-by sewage system lines.

A few of CBL’s shopping malls appear to be transitioning to home entertainment centers rather of standard retail shopping center as restaurant/bar, video gaming, and gym rents continue to increase. The issue for the staying merchants is that those going to the shopping center to operate at a health club or beverage at a bar might not be using their “shopping hat” – their function for going is really various than the foot traffic that is shopping. You might have a high level of foot traffic, however not buyer foot traffic in the shopping center. They are likewise using up parking areas that might make it more troublesome for real buyers.

A Take A Look At One Shopping Center – Brookfield Square

In order for financiers to get a much better “feel” for their particular residential or commercial properties I wish to concentrate on among their shopping malls – Brookfield Square, which CBL obtained in 2001. This shopping center was integrated in the mid-1960s in a residential area of Milwaukee and was among the very first totally confined shopping malls integrated in Wisconsin. The Brookfield/Elm Grove market location in the 1960s was primarily single-family homes with an upper-level management/professional head of family. The comfy homes had little or no home mortgages. When the shopping center opened it had Sears, JC Penney, Boston Shop, and T.A. Chapman’s as anchor occupants. There was really little other industrial realty in this quickly growing suburb.

Over the last 55 years, the marketplace location has actually considerably altered. The homes now frequently have 2 heads of family operating at mid to low level management/blue collar tasks with big home mortgages. This group modification implies less discretionary earnings per capita can be invested at Brookfield Square shops. The population for Brookfield/Elm Grove grew really bit from 2000 to 2020 (51,280 to 54,485). The population of Milwaukee is a sign of the rust belt decrease – went from 741,099 in 1960 to 577,222 in 2020.

Brookfield Square now just has JC Penney left as a significant anchor occupant. There are numerous other retailers that have actually been constructed for many years near the shopping center that contend for foot traffic. The whole location has actually been grossly over-built and there are a a great deal of retailer areas readily available to rent. The bad Brookfield Square $242 sales per square foot and 79% rented metric in 2022 shows these issues. To include insult, the variable rate of interest on the Brookfield Square protected option loan was 8.23% for 3Q 2023.

Current Outcomes

Before taking a look at the 3Q results it is necessary for financiers to keep in mind that CBL utilized “new beginning” accounting after they left Ch.11 in early November 2021, which affected some 2022 numbers.

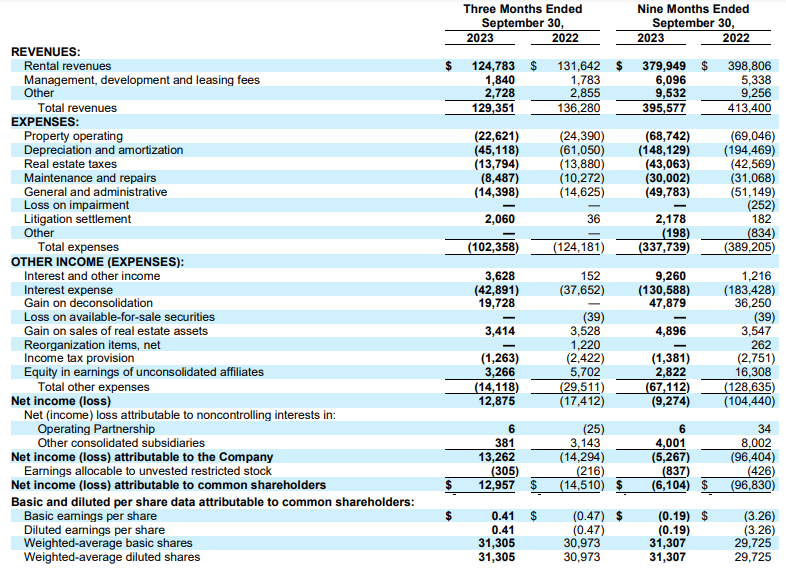

3Q and 9 Months Earnings Declaration 2023 and 2022

invest.cblproperties.com

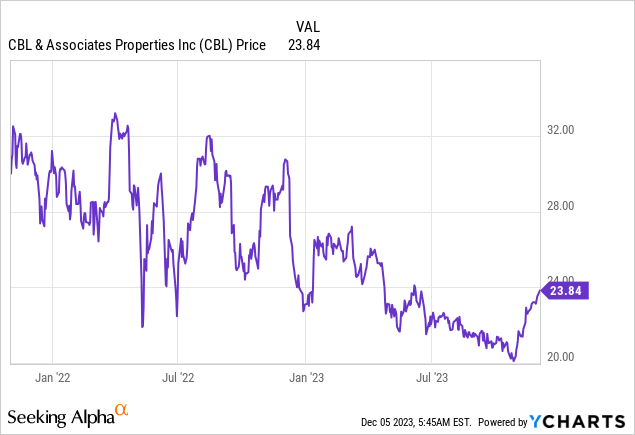

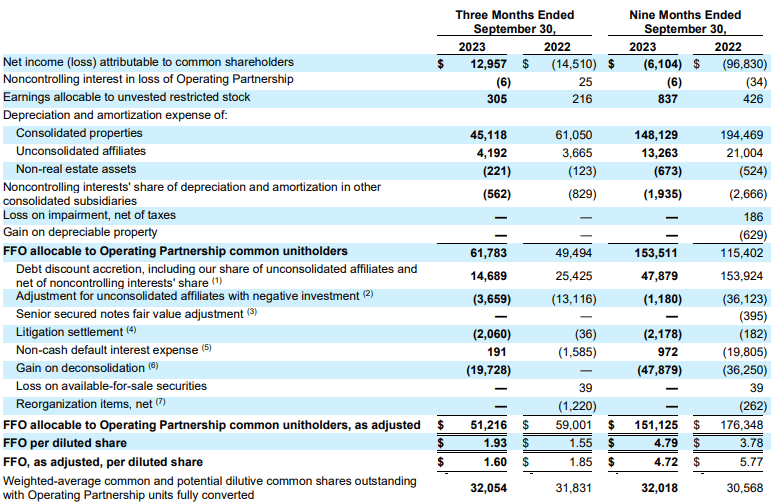

CBL’s stock rate has actually increased considerably over the last couple of weeks primarily since rate of interest have actually dropped (10-year UST yields dropped 80 basis points over the last 6 weeks) and not since of some particular enhancement for this REIT. Their 3Q outcomes were average. A couple of metrics enhanced, such as the overall portfolio tenancy rate increased by 30 basis indicate 90.8% and FFO per share increased to $1.93 from $1.55 in 3Q ’22. Some other metrics, nevertheless, relocated the incorrect instructions. Same-center NOI just increased 0.4% from 3Q ’22, which is less than the 3.7% inflation rate. Changed FFO reduced to $1.60 from $1.85. The metric that actually captured my eye was that the typical gross lease per sq. ft. decreased 4.0% in 3Q. This was really frustrating considering this was an intense area in 2Q23 when it increased an outstanding 9.1%.

FFO and Adjusted FFO

invest.cblproperties.com

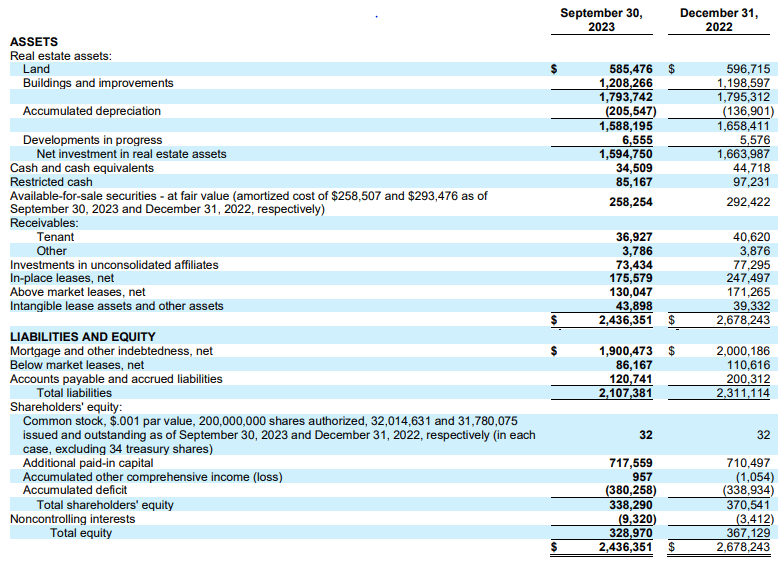

The balance sheet listed below is for completion of 3Q, however since November 2, the guaranteed term loan is now non-recourse. There is another metric that I discover unpleasant which is the overall financial obligation of $1,900 million minus overall cash/securities ($ 34.5 million + $85.2 million + $258.2 million)/ net financial investment realty properties of $1,595 million = 95.5%. Historically numerous realty properties have a market price considerably greater than their GAAP balance sheet numbers, however in some parts of the nation, such as the rust belt that is not constantly the case. I presume numerous REIT financiers looking for greater earnings are comfy with high GAAP accounting balance sheet utilize, however I am not. I likewise believe it was unreasonable for management to authorize the brand-new $25 million share redeemed program, particularly considering that they just have a ‘B’ provider credit score by S&P. As numerous readers currently understand, I am definitely versus share repurchases. The money must be utilized to minimize financial obligation or be paid as a dividend. Numerous REIT financiers are looking for dividend earnings holding a REIT and are not stock traders.

3Q and 9 Months Balance Sheet 2023 and 2022

invest.cblproperties.com

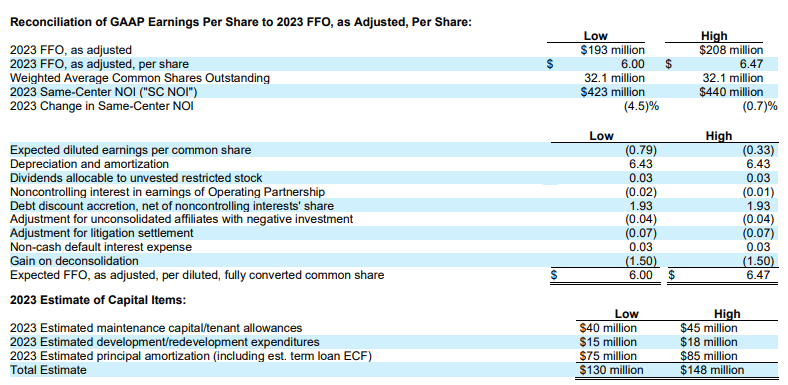

Management 2023 Assistance

invest.cblproperties.com

Why I am Not Suggesting CBL

My unfavorable viewpoint of CBL is based primarily on its long-lasting outlook. While CBL stock rate may increase decently if rate of interest continue to decrease, particularly considering that much of their financial obligation has variable rate of interest, there are other much better financial investments with brighter long-lasting outlooks that will likewise benefit near-term by lower rate of interest. Their present dividend yield of 6.28% is not that outstanding relative to UST note yields.

CBL has a lot of significant retail occupants with doubtful futures. If you purchase a shopping center REIT you are successfully purchasing a portfolio of merchants who are their occupants, and a lot of of their retail occupants I think about “offers”, such as Express. At this moment, I rate CBL a hold, however financiers ought to think about offering into any future strong rally from rate of interest cuts.