How Does the S&P 500 ESG Index Work?

Look under the hood of the sustainability-focused variation of the S&P 500 and find how index style affects diversity and efficiency.

The posts on this blog site are viewpoints, not suggestions. Please read our Disclaimers

Active or Agnostic?

In order to produce worth for his customers, an active financial investment supervisor need to differ a passive criteria– by selecting sectors, or designs, or specific stocks that the supervisor anticipates will surpass. The supervisor’s worth depends on the precision of his forecasts; the much better he is at recognizing the very best sectors, or designs, or stocks, the much better his outcomes will be. A passive supervisor, on the other hand, acknowledges his (actual) lack of knowledge about future returns

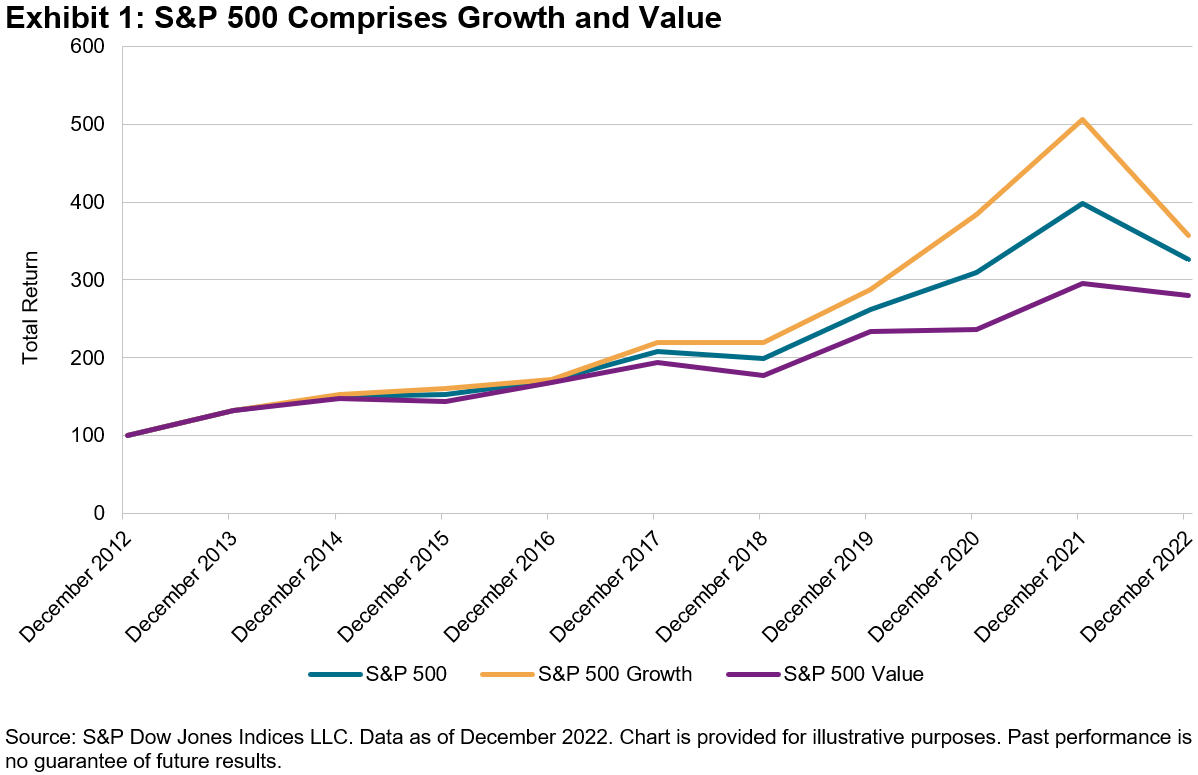

How precise do active forecasts require to be? How precise are they in practice? An easy idea experiment can assist check out these concerns: we’ll believe merely about turning in between development and worth as a way of surpassing the S&P 500 ® For the ten years ending in December 2022, the S&P 500’s overall return was 12.6%, while the S&P 500 Development and S&P 500 Worth indices returned 13.6% and 10.9%, respectively. Considering That Development and Worth combined make up the S&P 500, Display 1 is unsurprising.

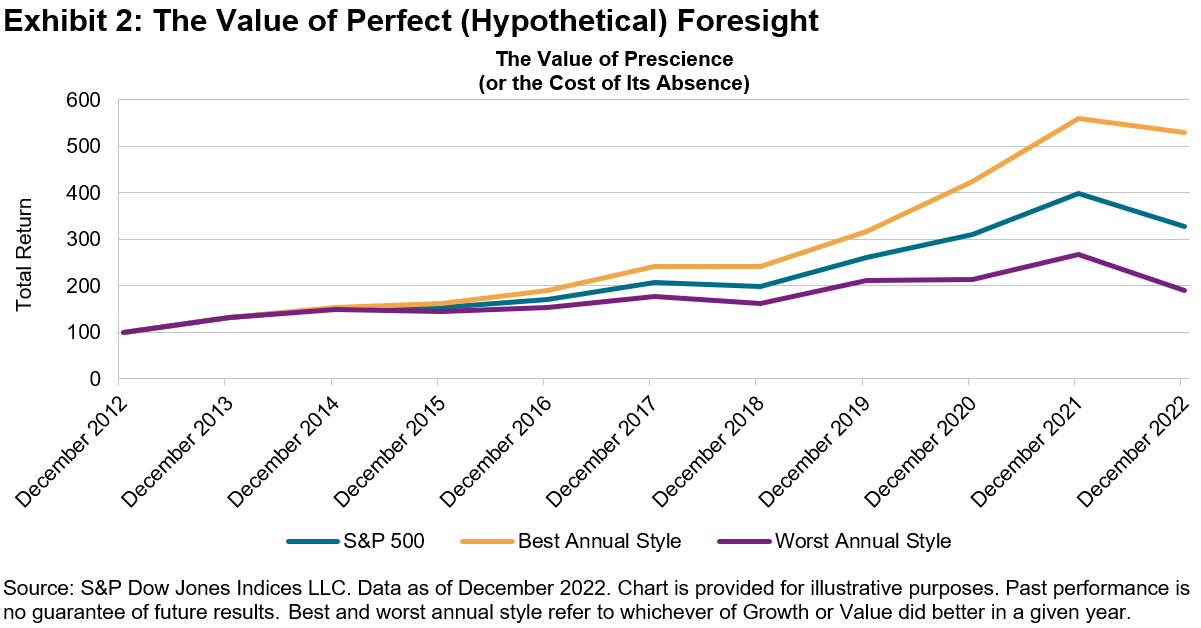

Expect, arguendo, that a financier moves every year to the design he anticipates will surpass. The limitations on such a financier’s efficiency are displayed in Display 2.

A financier who was right every year would hypothetically make a substance return of 18.2% for the duration; if he was incorrect every year the CAGR would be up to 6.6%.

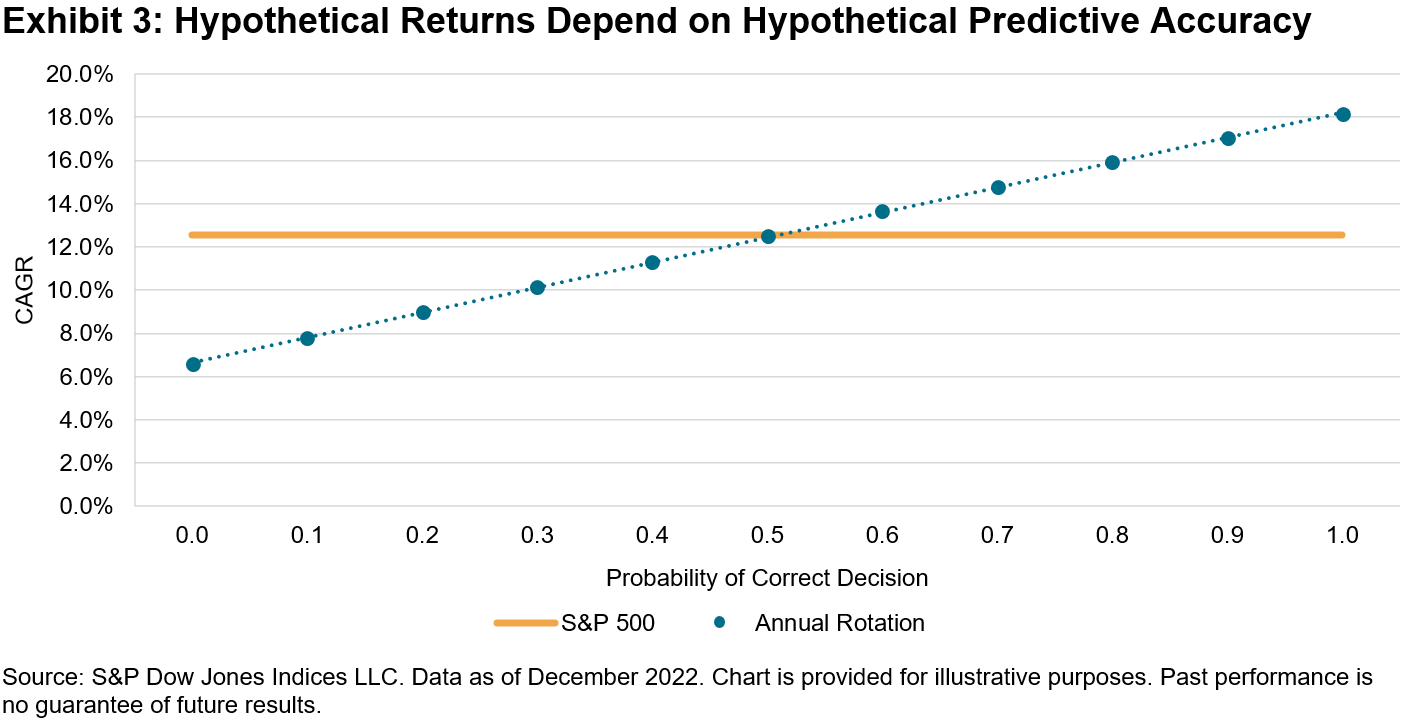

Naturally, it’s not likely that anybody attempting this technique in reality would be right– or inaccurate– every year. Display 3 demonstrates how the go back to a tactical rotational technique would differ depending upon the likelihood of making the right call. With a likelihood of 0.1, e.g., at the start of every year, the financier would have a 10% possibility of selecting the much better entertainer and a 90% possibility of selecting the even worse entertainer.

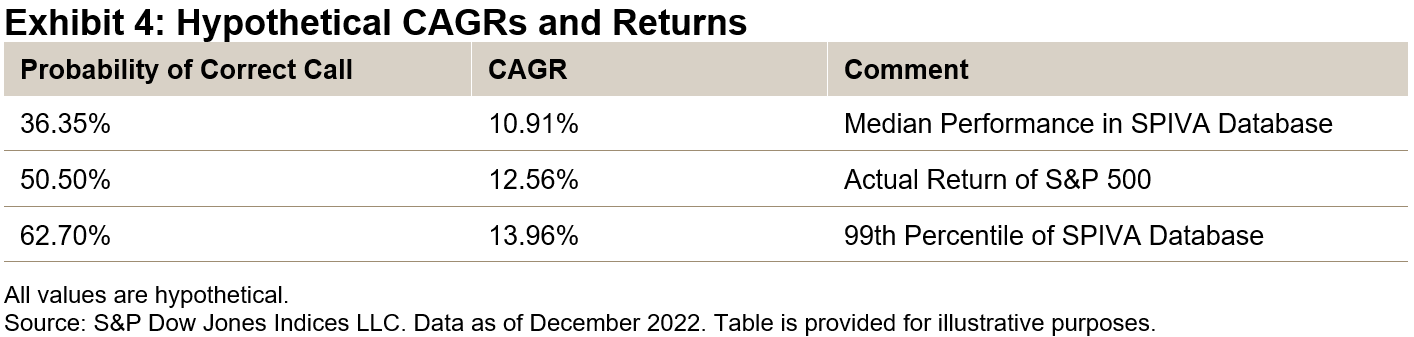

If every choice were best (likelihood = 1.0), the financier’s CAGR would be 18.2%; if every choice were incorrect (likelihood = 0.0), it would be 6.6%. What’s fascinating is to observe what occurs in between those limitations, as summed up in Display 4.

From these observations we can make some reasonings about the potential customers for effective design rotation:

- The efficiency of the typical large-cap U.S. equity supervisor in our SPIVA ® database (* )follows a 36.35% likelihood of making the best design call— i.e., even worse than a coin turn. Turning a coin would have produced around the return of the S&P 500, which would have suggested a top-quartile ranking for a large-cap U.S. equity supervisor. However if turning a coin is the very best you can do, it’s much better not to trouble and simply track the S&P 500.

- Predictive precision levels above 63% would have produced returns that no supervisor really produced, which suggests that no active supervisor had that level of predictive precision.

- Passive financiers can be comfy in their agnosticism.

The posts on this blog site are viewpoints, not suggestions. Please read our

Kieran Trevor

-

ESG

Tags -

carbon footprint,

carbon strength, environment modification, decarbonization, ESG, greenhouse gas, Net Absolutely No, Paris Arrangement, S&P 500 Net Absolutely No 2050 Paris-Aligned ESG Index, S&P PACT, S&P Paris-Aligned & & Environment Shift Indices, sustainability As the world intends to decarbonize towards a net absolutely no future, the value of tracking the carbon footprint of portfolios is ending up being a main focus for numerous financiers; particularly, to determine and comprehend whether portfolios replicate the emission decrease targets required worldwide to assist reduce the effects of environment modification.

For financiers, tracking an EU Paris-Aligned Criteria, such as

S&P 500 Net Absolutely No 2050 Paris-Aligned ESG Index, might supply a method to prevent the trouble, as the index embeds a preliminary 50% greenhouse gas (GHG) decrease and a minimum 7% year-over-year decarbonization rate in its building and construction, while traditionally keeping comparable efficiency qualities to the benchmark index. 1 In Between February 2021 and February 2023, the S&P 500 Net Absolutely No 2050 Paris-Aligned ESG Index minimized its carbon strength by 24.1%, beating its minimum necessary decarbonization of 13.5% because very same duration. The Industrials, Financials, Healthcare and Customer Discretionary sectors all decarbonized by over 30%, with carbon strength increases observed in Customer Staples, Realty and Interaction Providers. All Energy stocks were left out from the index throughout due to the index building and construction.

However how has this decarbonization been attained? We break this to discover the genuine motorists of the modifications in carbon footprint within the index.

Carbon Attribution

Initially, we divided the index into 3 different groups:

Inbound Positions:

- Representing constituents that just signed up with the index after February 2021; Outbound Positions:

- Representing constituents that were eliminated from the index in between the February 2021 and February 2023; and Kept Positions:

- Representing constituents that existed in the index considering that February 2021. Dividing the index into unique durations enables us to more properly associate how carbon entered the index and how it has actually been eliminated. In this case, a big percentage of carbon has actually been eliminated through divestment of business from the index, which represented a decarbonization of 32% (see Display 2) relative to the base-level carbon strength. On the other hand, brand-new business going into the index increased carbon strength by 4.9%, and business that kept their position in the index in both durations was accountable for an increase of 3%.

Next, we run a carbon attribution analysis on the kept positions to see what’s driving their net development in carbon strength. We observe that this was driven completely by weighting within the index, which offered the minimized count of general business in the index throughout this time from 358 to 313, makes instinctive sense. The interaction result in between a business’s weight and its carbon strength likewise helped in reducing the index-level carbon footprint. Business habits, represented by the real carbon strength modification of business in the index, had a reductive influence on general strength by over 15%.

Lastly, breaking this appealing pattern down even more by associating the strength modification, we observe that this result was driven in part by market conditions (EVIC), however mainly by emission decreases of these business, while the interaction result in between these 2 was very little.

Carbon attribution analysis can be an effective tool for market individuals wanting to decrease the carbon footprint of their financial investments, and it can be utilized to assist keep their decarbonization. Fortunately, the

S&P PACT ⢠(S&P Paris-Aligned & & Environment Shift Indices might supply a method to make this much easier, embedding a 7% year-over-year decarbonization rate by style and lining up with a net absolutely no future. 1

See S&P Paris-Aligned & & Environment Shift (PACT) Indices Approach for more details. The posts on this blog site are viewpoints, not suggestions. Please read our

Sherifa Issifu

-

Equities

Tags -

2023,

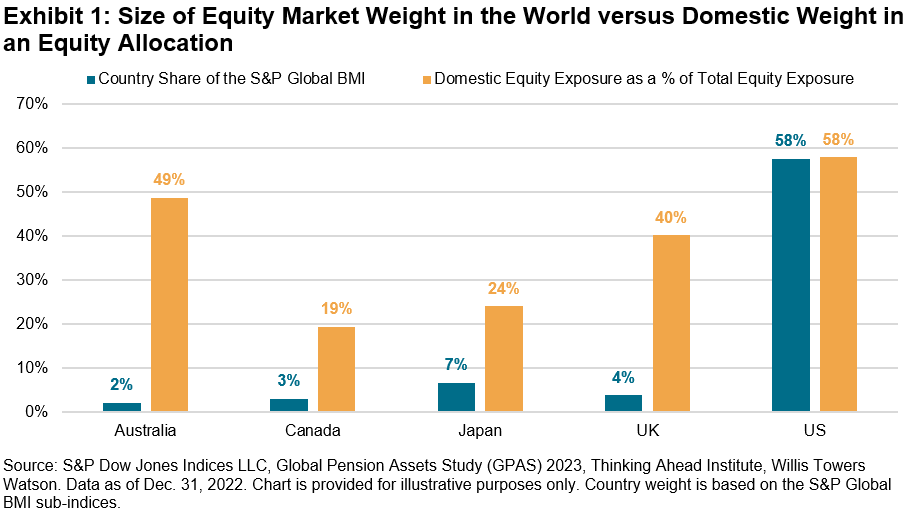

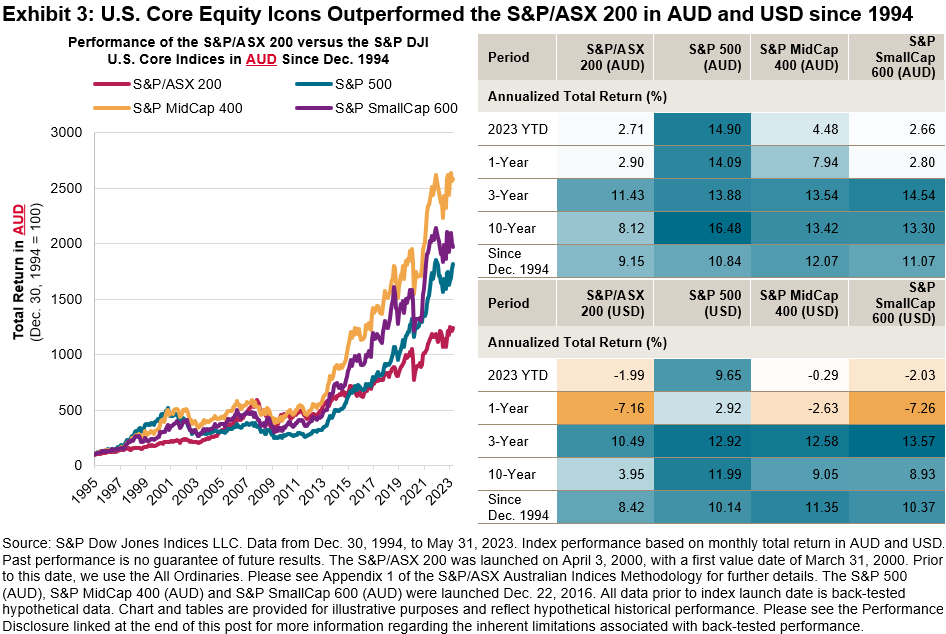

ASX, Australia, Australia FA, Australian equities, diversity, S&P 1500, S&P 400, S&P 500, S&P 600, S&P Composite 1500, S&P MidCap 400, S&P SmallCap 600, S&P/ ASX 200, Sherifa Issifu, U.S. Core, U.S. Equities Numerous market individuals have a “house predisposition,” generally having bigger direct exposures to domestic securities than would be identified by their representation in the international chance set. Australia is no exception: compared to Australia’s 2% weight in the

S&P Global BMI, Australian financiers assigned an approximated 49% of their overall equity allowance to domestic stocks at the end of 2022. 1 Display 1 reveals that Australia’s house predisposition– as determined by the distinction in between financiers’ overall domestic equity direct exposure and the nation’s weight in the S&P Global BMI– is bigger than numerous of its industrialized market peers, such as

Canada, Japan and the U.K. Such house predisposition implies that financiers have less direct exposure to the U.S. equity market, that makes up almost 60% of the S&P Global BMI. The

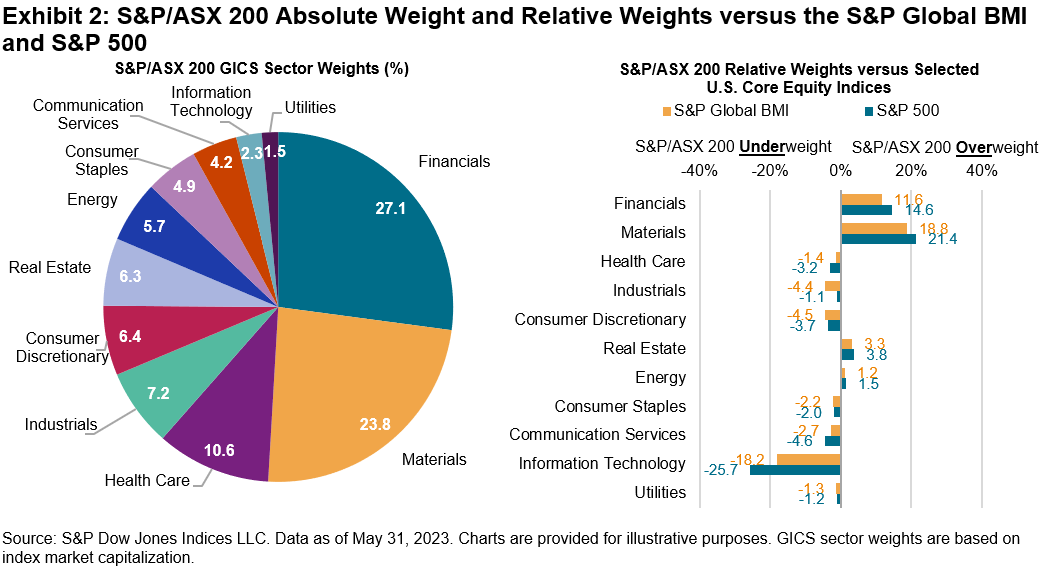

S&P Composite 1500 ®(* )represents the investable part of the U.S. equity market (~ 90%) by integrating the large-cap S&P 500 ® ,& S&P MidCap 400 ® and the S&P SmallCap 600 ® and neglecting less liquid and lower quality stocks. The U.S. is house to widely known international mega-cap names such as Apple and Microsoft, which might assist to stabilize Australia’s obese to Financials and Products. Display 2 reveals that integrating the U.S. and Australia’s equity standards might assist minimize the domestic sector predispositions. Compared to the S&P Global BMI, the Australian bellwether underweights Infotech by 18%, with I.T. being the S&P/ ASX 200

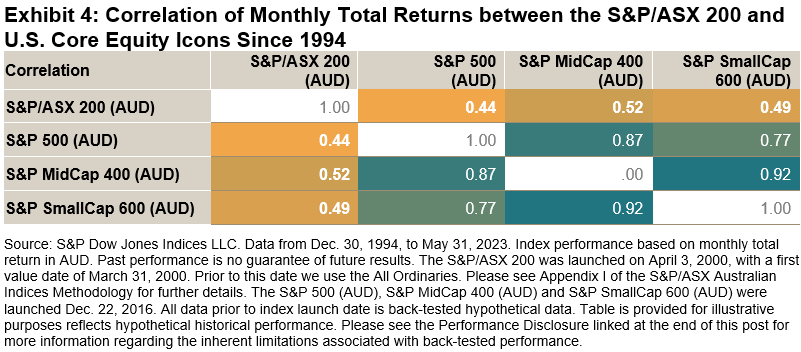

‘s second-smallest sector, at 2%. Possible diversity advantages might likewise have actually can be found in the type of enhanced risk/return profile. Display 3 highlights that the S&P 500 exceeded the S&P/ ASX 200 by 2% annualized considering that Dec. 30, 1994, in regional currency and U.S. dollar terms. This makes the long-run outperformance of the S&P 400 ®(* )and S&P 600

® much more outstanding; the non-perfect connections of these indices versus the S&P 500 (displayed in Display 4) likewise implies there is a chance for financiers to diversify within their U.S. equity direct exposure also to access to the special qualities of U.S. mid- and small-cap indices. Display 2 which reveals that distinctions in sector structure might assist describe the non-perfect connection in between the S&P/ ASX 200 to our U.S. core equity indices, which varies from 0.44-0.52 when taking a look at regular monthly returns in AUD terms, as shown in Display 4. This moderate connection recommends that integrating the 2 sets of indices might cause much better risk-adjusted return than either one in seclusion. In Display 5, we take the blue-chip standards of both the U.S. and Australia and develop theoretical mixes of the S&P 500 and the S&P/ ASX 200. We can see that including the S&P 500 to the S&P/ ASX 200 has actually traditionally enhanced return per system of danger (risk-adjusted return) throughout all points on the effective frontier over direct exposure to the S&P/ ASX 200 alone. While there are a number of reasons that Australian market individuals might pick to have a house predisposition, in the past, U.S. equities assisted financiers diversify from sectoral house predispositions and traditionally enhanced domestic returns.

1

Planning Ahead Institute, “

GPAS 2023 Pensions Study

,” 2023. The posts on this blog site are viewpoints, not suggestions. Please read our Disclaimers

Tags 2023, ASX,

S&P Dow Jones Indices

The financial obligation ceiling dispute in Washington seems nearing an end. According to the U.S. Treasury, Congress has “constantly acted when hired” and markets will search for them to do so for the 79

th

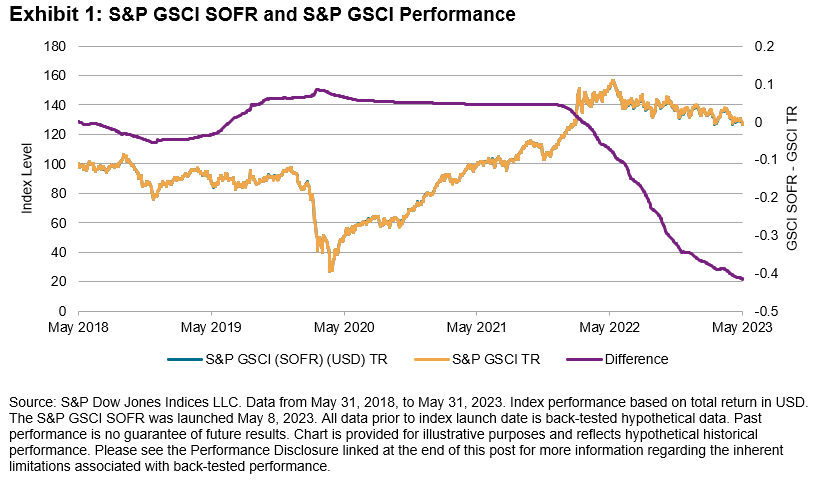

time this month. By index guideline, all products in the

S&P GSCI are sold U.S. dollars, so the value and respect to the “world’s reserve currency” rings real whenever a futures agreement on the S&P GSCI is settled. The S&P GSCI SOFR released in May and leverages the very same index building and construction and estimation concepts as the S&P GSCI, however uses the Safe Overnight Funding Rate (SOFR) into the estimation rather of Treasury Expenses. Utilizing SOFR in lieu of Treasury Expenses permits efficiency tracking with alternative money management techniques. Consisting of rates that are collateralized by Treasury securities, there is still direct exposure to the faith and credit of the U.S. federal government. Nevertheless, it omits particular deals that are considered to be trading “unique,” or at a rate outside the basic market activity. The SOFR is released daily by the U.S. Federal Reserve and can be discovered on its site. As SOFR volumes increase, the capability to have a complementary index permits possibly enhanced money management abilities through money and acquired instruments. Gold has actually long worked as the option to fiat currency when there is issue in the market concerning the political outlook. With this year’s dispute, the S&P GSCI Gold

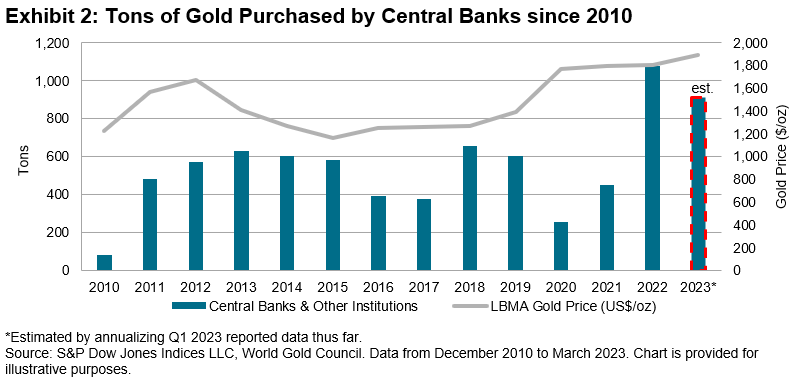

has actually traded near its all-time high and has actually exceeded broad products by over 18%. While fiat cash can, and likely will, continue to be printed, the international production of gold is fairly flat at simply 1% -2% of overall supply. Reserve banks have actually acquired gold at rates not seen considering that the U.S. federal government broke its gold requirement in 1971. Constant supply produces a fairly repaired base for the metal, while need is mainly driven by a few of the biggest holders of U.S. federal government financial obligation: international reserve banks.

Biggest Reserve Bank Purchases in 50 Years Because striking a YTD high of 12%, the S&P GSCI Gold has actually kipped down strong, if not magnificent, outcomes. Appeal has actually increased due to the current financial obligation ceiling arguments, and in spite of political leaders concerning a service that would prevent default, main lenders seem stockpiling. The posts on this blog site are viewpoints, not suggestions. Please read our

Disclaimers